MARKET UPDATE

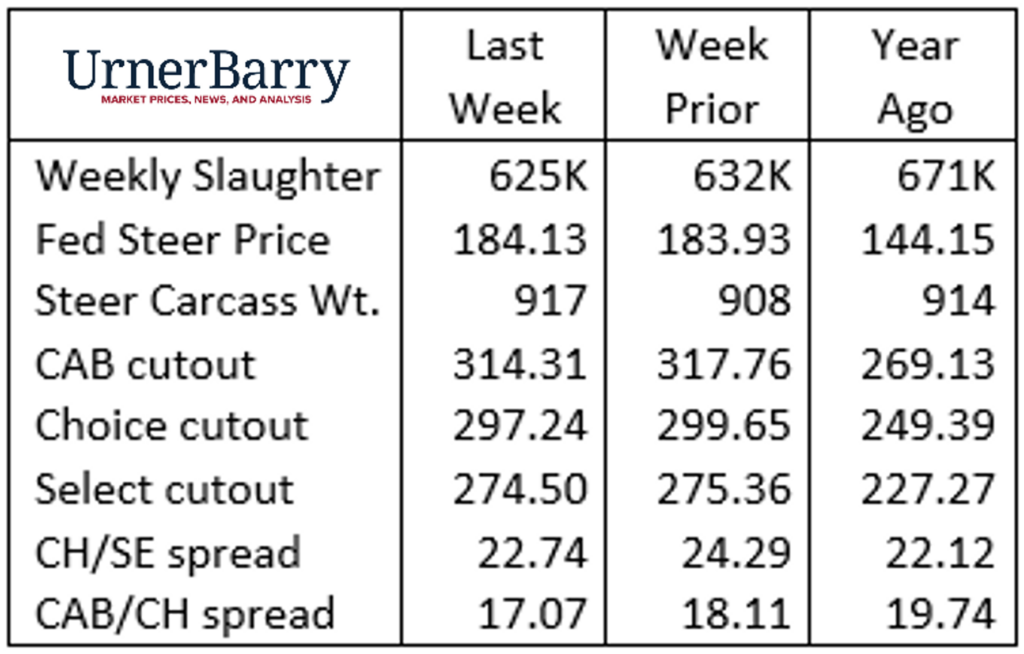

Federally inspected cattle slaughter last week was 7,000 head smaller than the week prior. This slaughter reduction aligns with the pace packers were targeting for the period. It’s normalized after two weeks of very low and high head counts due to the Labor Day week earlier this month.

The north-to-south price differential narrowed again last week as a potential signal that currentness in fed cattle supplies is leveling up between the major trade regions. Southern feedyards traded for $183/cwt., while Nebraska/Iowa feedyards traded between $184 and $186/cwt.

While the market average trading range has narrowed from the recently historically wide range, the total market average in the six-state region has priced in a fairly tight range in the low to middle $180’s since the middle of June. The comprehensive cutout traded in a range from $325/cwt. to $301/cwt. in the same period.

Carcass cutout values were lower again last week with some narrowing of the price spreads as well. Expect cutout values to reach their seasonal lows by the second week of October before catching fourth quarter demand traction, rallying in early November. Price declines on chuck cuts enticed buyers last week as retail interest tends to increase for these items looking ahead to October and November. Ribeye prices were slightly higher last week as buyers continue to store inventory in the “near frozen” state to achieve needed supplies for the holidays. Spot market ribeye prices represent a small available supply for this reason and the price pattern is strongly higher this year compared to the past two years.

Other noted trends we’ve been tracking continue on a firm pattern in latest data. Seasonally lower values on strips and shortloins are on the expected pace. As well, sharply higher 90% lean trimmings prices are holding the alternative round cuts from fed cattle on a higher plane as we’ve recently pointed out.

CARCASS WEIGHTS SURGE, CHOICE GRADE SETBACK

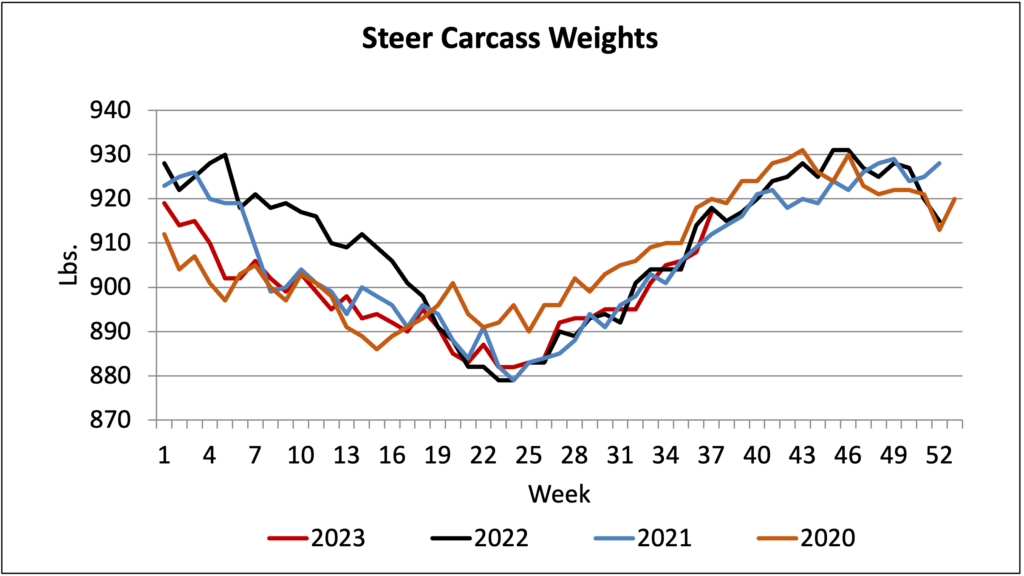

In the past 10 years steer carcass weights reached their annual lows in the third week of May and touched their heaviest annual mark in the second and third full weeks in November. Since the COVID interruptions in 2020, the spring lows have migrated into the month of June.

The magnitude of change in steer carcass weights from the spring-low to the fall-high in each of the past five years has been relatively close, except for 2019. The August 9, 2019 fire at Tyson’s Holcomb, Kansas plant set industry slaughter efficiency back, generating heavier than normal weights into the fall, aggregating a 70 lb. weight swing from the spring low to the November high. The second largest weight swing in the series was a 58 lb. seasonal increase in 2018 with the remaining years posting no less than a 45 lb. change.

The first four months of 2023 saw average steer weights fall 15 lb. short of a year ago due to exceptionally poor winter-feeding conditions. Since early May steer weights have adjusted higher and have since averaged just 1 lb. heavier than in 2022. Major contributors are slower slaughter throughput and less current finished cattle supplies in the south. Latest data for the week of September 3 shows steer carcass weights surged 9 lb. to average 917 lb. each. This is large jump given that weights had only moved up 13 lb. total in the five previous weeks. It’s important to factor carcass weight changes to understand production tonnage as we discuss weekly head counts and throughput. The single-week 9 lb. per head increase equates to multiple semi-loads of boxed beef production.

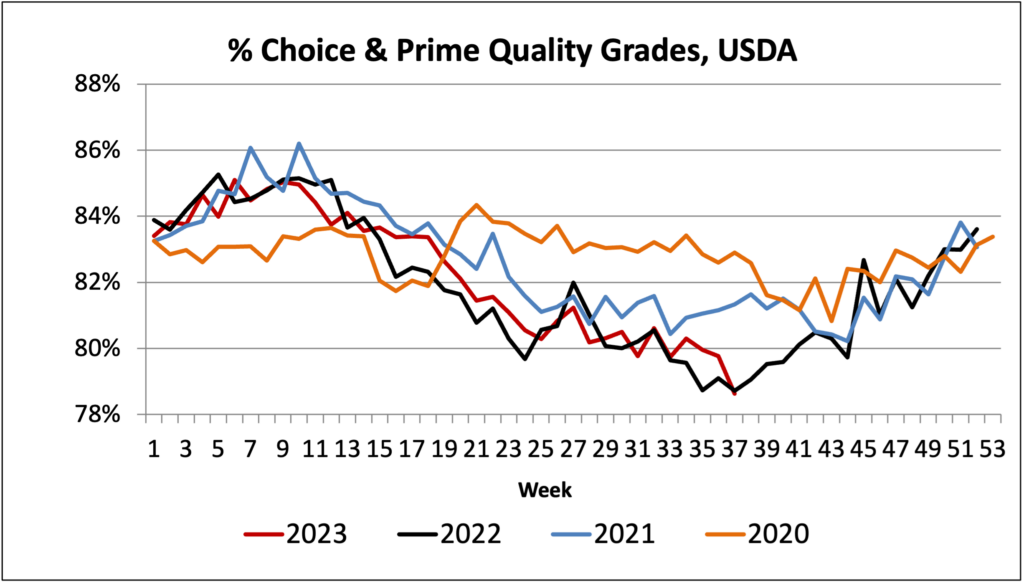

Heavier carcasses typically coincide with richer marbling and higher quality grades. But seasonal grade trends simply push quality lower this time of year as USDA’s grading report for the September 11 week shows an abrupt leg down in percent USDA Choice. The one percentage point single-week drop placed the Choice share at 70.3% of steer and heifer carcasses. While this may seem like a small shift, it’s truly sizeable since the annual Choice percentage has trended within just a five-point range annually in recent years.

Latest data for the national Prime grade shows the current 8.27% holding a bit higher than the 7.6% for the same week last year. Combined Choice and Prime grade shares are currently even with their position a year ago today, which was the lowest quality grade performance week of the year.

Surprisingly, the Premium Choice branded share of the Choice grade appears relatively unaffected. The category even shifted fractionally higher amidst the Choice downturn to average 30.9% of the Choice product total. Certified Angus Beef is the largest component of the Premium Choice branded offering. The brand’s latest carcass acceptance rate near 32% is 1.5 points higher than a year ago as that figure seeks to mark the fall low very soon.

Read More CAB Insider

Seasonal Carcass Impacts

An overriding theme across the past 18 months in the beef sector has been increased carcass weights. In general, fed steer and heifer carcasses averaging 25-30 lb. heavier year over year has been a net positive for the industry.

Margins Sqeeze, Markets Cool: What It Means for Fed Cattle

Focused marketing of a premium beef brand demands some attention to tracking price spreads across differing quality specifications. The USDA quality grade scale provides the domestic measuring stick by which the trade differentiates demand across the quality spectrum.

Rapid Decline in Select Carcasses

The steep upward price trajectory in the fed cattle market remains wholly supported on fed cattle remaining in tight supply and the tight grasp of cattle feeders keeping feedlot stays and carcass weights elevated. Weights continue to underpin beef production tonnage, cutting the harvest pace deficit for fed cattle.