MARKET UPDATE

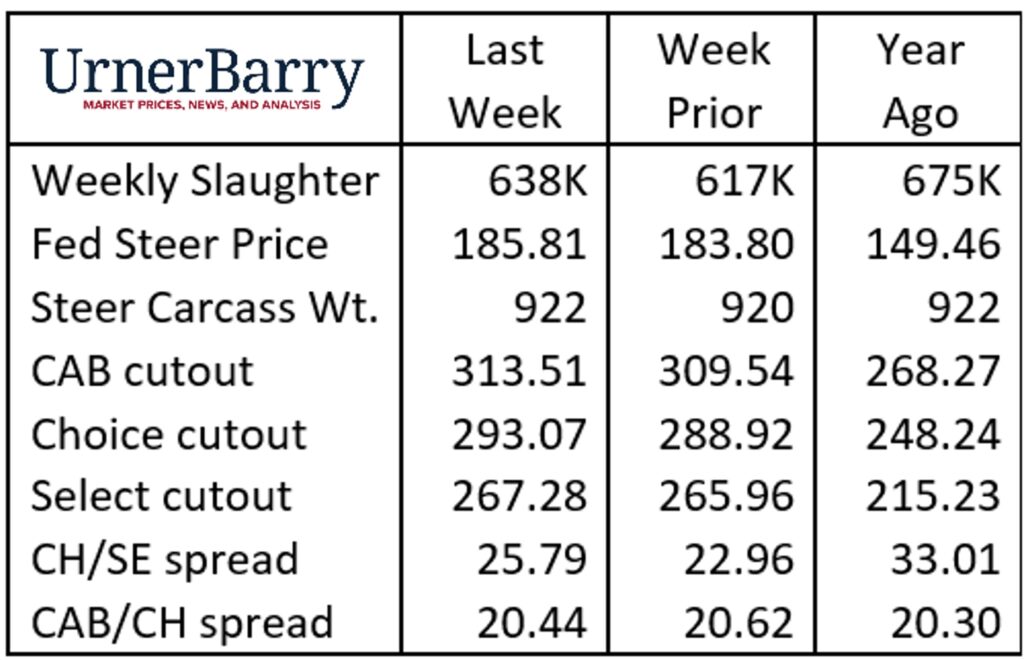

Last week, fed cattle slaughter saw a bit of recovery with a 638,000 head weekly total. Singling out the fed cattle slaughter shows Friday’s total was reduced just 8,000 head compared to the average daily total in the four prior business days that averaged 98,750 head each.

In the previous week, negotiated fed cattle traded in a range between $185-$186/cwt. last week in a market that denoted a much firmer tone than it had for many weeks. This price level was the highest since early August in a market that has been tightly rangebound for multiple weeks.

The October 1 Cattle on Feed report, published last Friday, is the most impactful short-term market factor at this time. Feedlot placements for September were unexpectedly 106% of placements a year ago, contrasted against varied analyst pre-report estimates for placements just over 100%. December Live Cattle futures, which closed Friday at $184.60/cwt., ended Monday’s session at $178.35/cwt., a $6.25/cwt. decrease). In a volatile, short-term scenario, Live Cattle contracts began to recover some of the lost ground by Tuesday morning.

Meanwhile, current cattle and beef market fundamentals are positive. Packer demand for cattle was sharp last week with the $2/cwt. price increase on a significant volume of negotiated cattle. Total USDA Choice carcass production is 8% lower than a year ago in the latest weekly report, driven lower on a one percentage point decline in the Choice grade.

As well, cutout values have turned the corner with higher weekly average values across the board last week with CAB up $3.97/cwt., Choice up $4.15/cwt. and Select $1.32/cwt. higher. As we had mentioned two months ago, the dip in total USDA Choice boxed beef tonnage was destined to hit the fourth quarter market with widening Choice-Select price spreads. That is evident in our latest data with the Choice cutout $25.79/cwt. premium to Select. The CAB/Choice price spread is more stable at $20.44/cwt., which is historically wide but perfectly aligned with October price spread values since 2020.

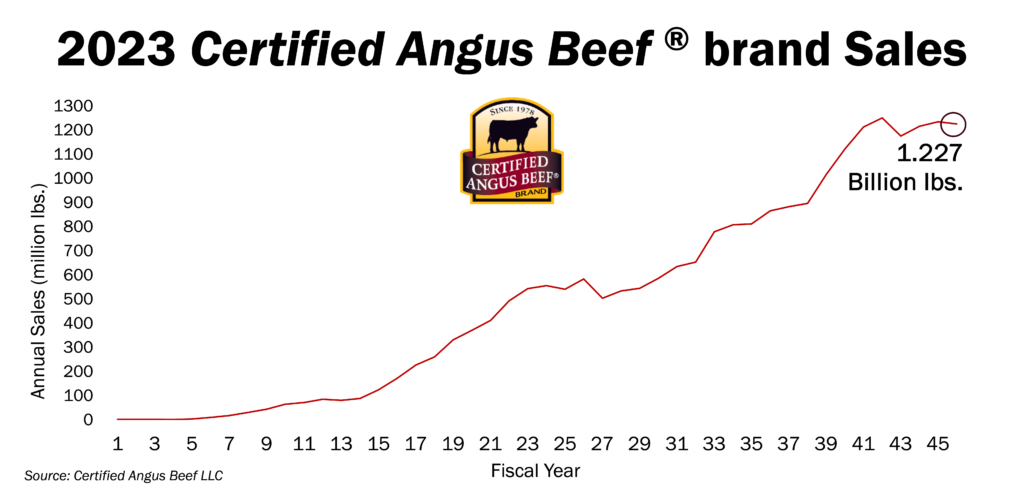

CAB Brand Sales Third Best in 45-Year History

Shifting market dynamics have already marked trend changes in the 2023 cattle and beef markets. These shifts are most succinctly summarized through two factors, fewer cattle and higher prices, that will further entrench themselves in near term trends.

As Certified Angus Beef celebrated the close of its 45th year this September, several highlights emboldened brand stakeholders and producers. The single largest factor in the brand’s supply, fed cattle slaughter volume, provided a formidable obstacle as the nation’s drought-reduced cow herd pulled fed cattle supplies 3.3% lower for the past 12 months. However, with other positive trends, CAB acceptance increased 0.5% for the fiscal year with 5.82 million head earning the CAB brand.

Marbling trends have been on a lower pattern in the past year with USDA Choice slightly lower for the period. However, the Premium Choice carcass share has been surprisingly strong. This, coupled with the Prime grade working both above and below the 2022 pattern, allowed the CAB carcass acceptance rate to improve half of a percentage point to 36% in fiscal 2023.

Cattlemen continue to include Angus genetics in their breeding programs to a greater degree, boosting brand-eligible cattle to more than 72% of total fed cattle supplies. This includes enrichment from the heavily Angus-influenced beef x dairy population. There were 16 million Angus-type carcasses processed at licensed packers in the fiscal year, roughly 72% of the fed steer and heifer supply.

CAB brand sales battled the headwind of smaller steer and heifer slaughter to end the year just 0.5% lower than in the 2022 fiscal year. This culminated in the third-largest sales volume year and the eighth year of brand sales surpassing one billion pounds.

While retail grocery store sales were understandably 4.9% lower on the year there were several notable highlights on the positive side of the ledger. International brand sales were up 6% with largest gains in China, Hong Kong, South Korea and Mexico even though total U.S. beef exports charted a negative trend. Record-large CAB Prime sales featured a 17.7% increase while value-added products were up 9.8%. Both categories surpassed 40 million pounds of CAB sales volume.

Fourth quarter trends are currently widening quality carcass price spreads with the Choice/Select spread at $25.79/cwt. and the CAB/Choice spread at $20.44/cwt. Short-term packer demand for quality cattle to fulfill demand for traditional CAB and CAB Prime carcasses should result in continued expanded grid premiums through early December. Although surprisingly larger feedlot placement head counts were reported for September, continued high-quality carcass supply challenges will remain a theme in the brand’s 46th year, already underway. This recommends cattlemen in each sector maintain focus on carcass demand factors and the margin opportunity that exists for cattle to meet modern consumer expectations.

Read More CAB Insider

Seasonal Carcass Impacts

An overriding theme across the past 18 months in the beef sector has been increased carcass weights. In general, fed steer and heifer carcasses averaging 25-30 lb. heavier year over year has been a net positive for the industry.

Margins Sqeeze, Markets Cool: What It Means for Fed Cattle

Focused marketing of a premium beef brand demands some attention to tracking price spreads across differing quality specifications. The USDA quality grade scale provides the domestic measuring stick by which the trade differentiates demand across the quality spectrum.

Rapid Decline in Select Carcasses

The steep upward price trajectory in the fed cattle market remains wholly supported on fed cattle remaining in tight supply and the tight grasp of cattle feeders keeping feedlot stays and carcass weights elevated. Weights continue to underpin beef production tonnage, cutting the harvest pace deficit for fed cattle.