2018 Year in Review

More demand for more of the best

By: Paul Dykstra

The past year in beef cattle markets may be characterized best by two very important factors. Not surprisingly, those are supply and demand.

While the U.S. beef cow herd remains in expansion mode, the pace has greatly slowed as seen by the share of heifers in the fed cattle mix. That number moved up to average 35%, but still lower than the 36-37% rate that typifies a liquidation phase. Projections were for the beef cow herd to be at least 9% larger on January 1 this year, than the drought-induced cycle low of 29.1 million head in January 2014.

Smaller inventories of fed cattle going back to the turn of the century spurred packers to begin reducing capacity a dozen years ago. That brought the industry to its current position of restricted processing capacity in the face of a now increasing fed-cattle supply.

One result was three years of exceptional packer profitability, increasing in each of those years to record levels in 2018. Even so, those very profit margins enticed packers to maximize production, processing an additional 7,000 head per week to average 497,000 fed steers and heifers. Expectations are for 2019 to bring on another 1% increase in fed-cattle harvest counts.

Though a continuation of 2017 trends, the magnitude of increase in packer leverage underscored the 2018 market. The cattle feeders’ share of wholesale beef values plunged to a record of just 50% last May, according to market reports from Urner Barry and CattleFax. That ratio of 2 to 1 beat the June 2017 peak ratio of 1.88 to 1.

Fed cattle prices traded in a smaller range in 2018, posting a lower average price for the third year in a row at $116.69/cwt., live basis, compared to the prior year’s $121.10/cwt. The 2018 market top came in February at $129.75/cwt., leaving the much-anticipated 2nd quarter high a bit shy of expectations at $124.81/cwt. during the first week of May. One highlight for cattle feeders was that the annual price low came in $2/cwt. higher than the prior year at $106.87/cwt. during the last week of June.

The range in fed cattle price was also much narrower in 2018 with a top-to-bottom spread of $22.88/cwt. That’s in contrast to the much wider range of $39.94/cwt. the prior year, dominated by a market-shocking void of finished cattle during the high-demand period of early May.

- 2006 Choice 51%

- 2017 Choice 72%

- 2018 Choice 71.5%

Adjustments to camera-assisted USDA quality grade lines in late 2017, immediately followed by adoption of dentition-based carcass maturity calls had feeders and packers eyeing year-on-year grading trends in 2018. The close proximity in time of those two changes likely obscures the opportunity for those outside of the packing industry to clearly link causes and effects. Even so, the culmination of several factors that affect marbling scores certainly shifted quality grade shares.

Continuing the trend since 2006, U.S. averages for quality grade improved. The proportion of Choice carcasses had climbed from that 2006 low of 51% of all fed-cattle carcasses to a 2017 high of 72%. The consistently larger Choice category finally relented in 2018, but just half a percentage point (0.5 ppt). And that baby step backward was part of the ongoing historic move toward higher quality carcasses as a significant rise in Prime carcass production stole the show.

From 2000 through 2013, there was little variation in the proportion of Prime carcasses in the mix, ranging from 2% to 3.5%. Prime was so scarce, not many gave a thought to the richly marbled grade outside of high-end restaurants and a scant few retailers. Cattle feeders certainly didn’t consider Prime grid premiums as a significant component of normal production. Until the last few years, Holstein steers made up as much as 50% of Prime, so the remainder from native beef sources was rightly considered incidental in the big picture.

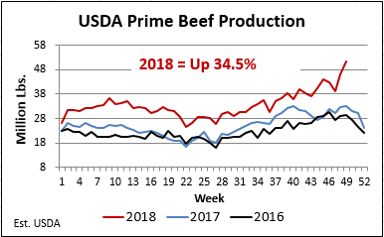

Just five years ago the proportion of Prime carcasses began to grow, inching up to 4% in 2014, adding another point in 2015 and resting at 6% for each of the next two years. Quietly doubling the Prime grade category in a short handful of years was progress, for sure, but few noticed the significance until 2018 when that exalted grade reached 7.8% of fed-cattle production. Rising 1.8 ppt may still seem small to some, but that’s a 35% tonnage increase in 12 months.

This rapid advance in Prime beef availability left its premium above Choice boxed beef unshaken through 2017. In fact, that year saw one retailer’s huge spring buy of Prime beef in a forward-purchase arrangement spark a supply problem for other end users, pushing the annual Prime cutout premium to $31.26/cwt., compared to a $25/cwt. average for the previous two years.

However, 2018 featured no market-moving purchase while the Prime category grew by 35%, bringing the annual Prime-Choice price spread to just $13.96/cwt. on the cutout. Similarly, the spread between USDA Prime and all USDA branded beef products narrowed to $9.05/cwt., down from the prior year’s $25.84/cwt.

The caveat for the 2018 price comparison is that “USDA branded” included a larger proportion of Prime-graded beef last year as well. The Certified Angus Beef ® (CAB®) brand enjoyed a 31% sales volume increase in its extension CAB brand Prime category, while total sales for the company were up 8% in Fiscal 2018. CAB sales data shows multiple weeks with Prime comprising over 10% of total sales—thus the Prime-to-“branded” price comparison is a bit skewed for the year-on-year picture.

Premium Choice branded products were also more prominent in 2018 with the share of Choice production captured by these brands up to 31.5% by early December, 2 ppt. higher than in 2017. That was another function of stronger marbling trends pushing more carcasses over the important line from “Small” to “Modest” marbling, the entry point to Premium Choice.

At roughly 85% of the Premium Choice branded market, the CAB brand was on track by year’s end to garner a 3-ppt. increase in Angus-type cattle accepted. Two-thirds of fed steers and heifers fit the “Angus-type” description last year, a 2-ppt. increase on 2017. Coupled with a 1.5% larger fed-cattle supply, that created a 5% increase in eligible cattle presented to graders for evaluation under the brand’s 10 carcass specifications.

“We should embrace this shift, the fruit of a logical market response that will guarantee beef remains the preferred protein.”

Paul Dykstra

The narrower Prime cutout premium saw average packer grid premiums for Prime carcasses decline. Although the year began with a 1st quarter average above $16/cwt., by the typically high-quality 3rd quarter’s larger supplies eroded the Prime premium to $11.80/cwt. versus $18.14 for the same period in 2017. The trend continued with the 4th quarter Prime premium of $10.23/cwt. down $5 in a year. CAB brand grid premiums, however, pulled slightly ahead in the second half of 2018, the $4.11/cwt. average up 13 cents on the same period in 2017.

A smaller Prime premium creates momentary demand concern for some producers, especially if they have taken steps to ramp up supply. However, even at a $9 or $10/cwt. premium on a carcass basis, those Prime carcasses are still worth $75 to $85 per head more than a Choice carcass at 860 pounds (lb.) carcass weights. Moreover, as end users become more accustomed to the affordable availability, there will likely be more uptake and commitment at their level to feature Prime grade beef in meat cases and on menus.

This can only help our industry firm up its place at the head of the table in protein competition. With U.S. pork and poultry in record supply and not likely to decline, we’re seeing a record-wide price margin favoring beef above the two. CattleFax data says demand for Choice and higher grading beef has increased even as supplies rebuilt from the deficit of 2014, led most significantly by increases in Choice and Prime availability. The message is clarified when we note the decline in both production and demand for Select and lower grade beef, more easily replaced by cheaper pork and poultry.

We need not fear a market more saturated with high-quality beef. Rather, we should embrace this shift, the fruit of a logical market response that will guarantee beef remains the preferred protein.

This story by Paul Dykstra originally ran in the Angus Beef Bulletin in March 2019.

You may also like

The Angus Argument

There’s no denying CAB has helped dramatically expand the market share for registered Angus genetics. Arguably, that success has encouraged several other breeds to adopt a black hide color by incorporating registered Angus genetics into their breeding programs and registries.

From Decline to Dominance

Initiated from a simple yet visionary idea, and pursued through the grit and tenacity of Angus breeders seeking a better future for the breed and Association members, it’s no accident that Certified Angus Beef is where it is today.

Smitty’s Service on CAB Board

Lamb continues to find himself struck by just how far-reaching the Angus breed has become. The brand’s growing demand and rising prime carcasses left a strong impression. He hopes everyone recognizes the vital connection built between consumers and Angus producers. Humbled by the opportunity to serve, Lamb reflects on his time as chairman with gratitude.