MARKET UPDATE

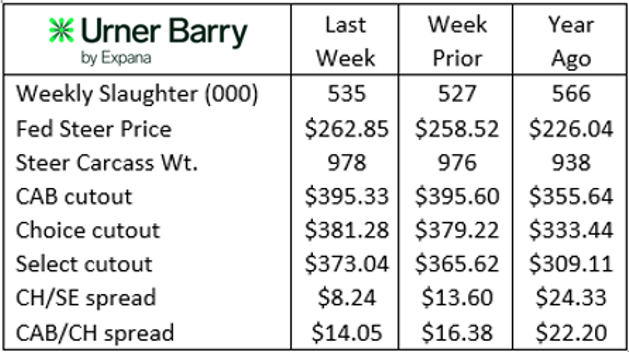

The run-up in fed cattle prices over the past four weeks has been impressive with a $16.67/cwt. live steer inflationary trend culminating in last week’s $262.85/cwt. steer price.

Federally inspected harvest head counts have also improved to fulfill larger boxed beef sales commitments on spring grilling and holiday demand. The past three weeks have averaged 532,000 head weekly counts compared to the 516,000 head average in the prior three weeks.

The steep upward price trajectory in the fed cattle market remains wholly supported on fed cattle remaining in tight supply and the tight grasp of cattle feeders keeping feedlot stays and carcass weights elevated. Weights continue to underpin beef production tonnage, cutting the harvest pace deficit for fed cattle.

Cash cattle values have run higher with no support from boxed beef prices as the Comprehensive cutout has been relatively stagnant for the past six weeks—after pulling back from the March highs. Wholesale prices are expected to adjust higher into June, in keeping with previous seasonal trends, but this has yet to develop.

June Live cattle futures remain a deep discount to cash, trading at a $10.95/cwt. below the latest cash prices as of Wednesday morning. At this point in May, plenty of time remains for the June contract to converge with cash.

Forward contract feeder calf video sales have kicked off this week with a portion of producers pulling the trigger earlier than normal, capitalizing on the current market and offsetting risk. Fall delivery calf prices are showing breakevens calculated against the current record-high cash fed cattle market. CME Live Cattle contracts for next spring are nearly $30/cwt. behind today’s cash; this suggests that buyers are both “betting on the come” and planning to add significant cheap gains to back up total cost.

More on Price Spreads

In April we discussed the notable shift in the spring Choice-Select price spread as the Choice premium dropped to nearly $0.00/cwt. in spot market pricing. The trend has extended into May with the spread remaining well below $5/cwt. with numerous excursions with the Select cutout becoming premium to Choice.

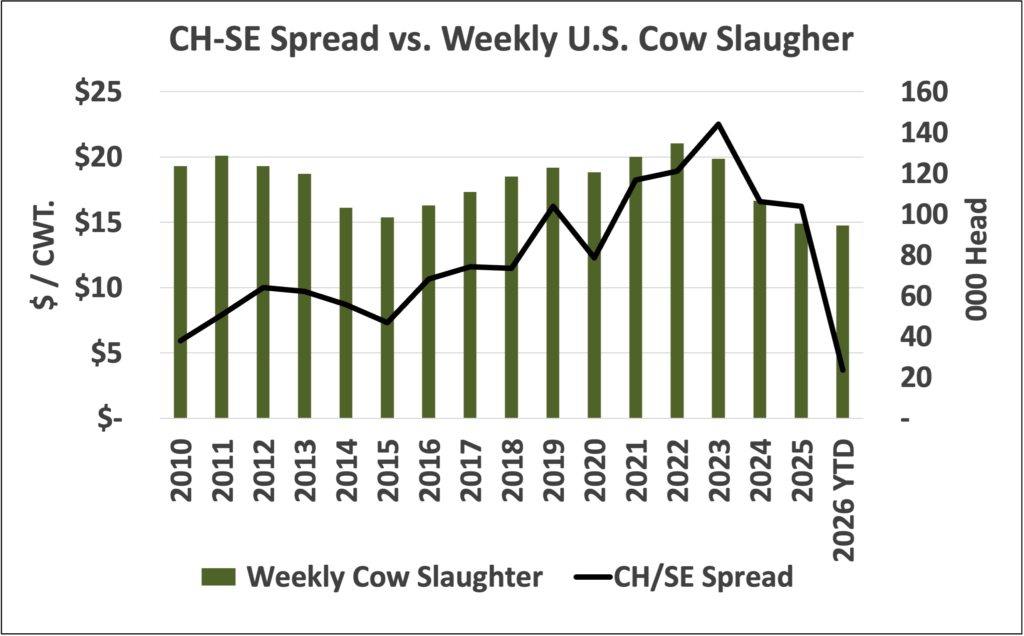

Market analysts have appropriately focused on the rapid decline in Select carcasses, dropping from 12% of the fed cattle mix in December to average just 8% since February. This historically small Select share has created a scarcity in the category compared to the lower 1/3 Choice price, which is literally what’s left in the Choice box after Premium Choice brands, like Certified Angus Beef ® , have been marked up for a premium end point.

When considering the higher Select value, this year’s exceptionally small cull cow harvest is also important domestic ground beef demand is quite strong, with more than half of beef consumption in this category. The chart shows the relationship of the Choice-Select spread with weekly cull cow harvest since 2010. It’s clear that the cyclical trend of cow harvest has been closely aligned with the fluctuations in the Choice-Select price relationship. As cow harvest declines the value of lean, Select end meats increases as those cuts become attractively priced in relation to lean cow cuts. It’s a simple substitution effect as 90% lean trim inflates in value under supply constraints.

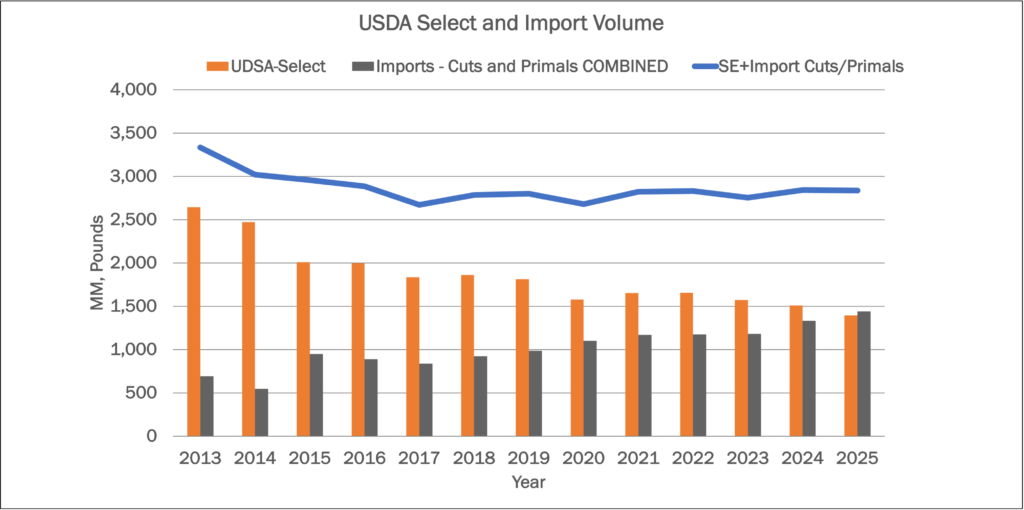

The second chart depicts the relationship of Select carcass supplies versus imported beef. Since the majority of imported beef is lean trim, destined to be ground a blended with 50% domestic lean trim, there is a clear relationship. As Select carcass supplies have declined, the imported tonnage has increased to replace tonnage while the market seeks to maintain balance in lean beef supply. Adding in domestic cull cow supplies to this chart would further illustrate how all three sources of lean beef volumes adjust to supply a relatively steady volume of ground beef for domestic consumption.

In contrast to the lean beef discussion, Certified Angus Beef ® brand cutout values have performed within expectations so far in 2026. The CAB cutout has averaged $17.63/cwt. above USDA Choice since January, just $0.90/cwt. lower than the same period last year.

Read More CAB Insider

Seasonal Carcass Impacts

An overriding theme across the past 18 months in the beef sector has been increased carcass weights. In general, fed steer and heifer carcasses averaging 25-30 lb. heavier year over year has been a net positive for the industry.

Margins Sqeeze, Markets Cool: What It Means for Fed Cattle

Focused marketing of a premium beef brand demands some attention to tracking price spreads across differing quality specifications. The USDA quality grade scale provides the domestic measuring stick by which the trade differentiates demand across the quality spectrum.

Beef Month Anticipation: Cattle and Beef Values

MARKET UPDATE...