MARKET UPDATE

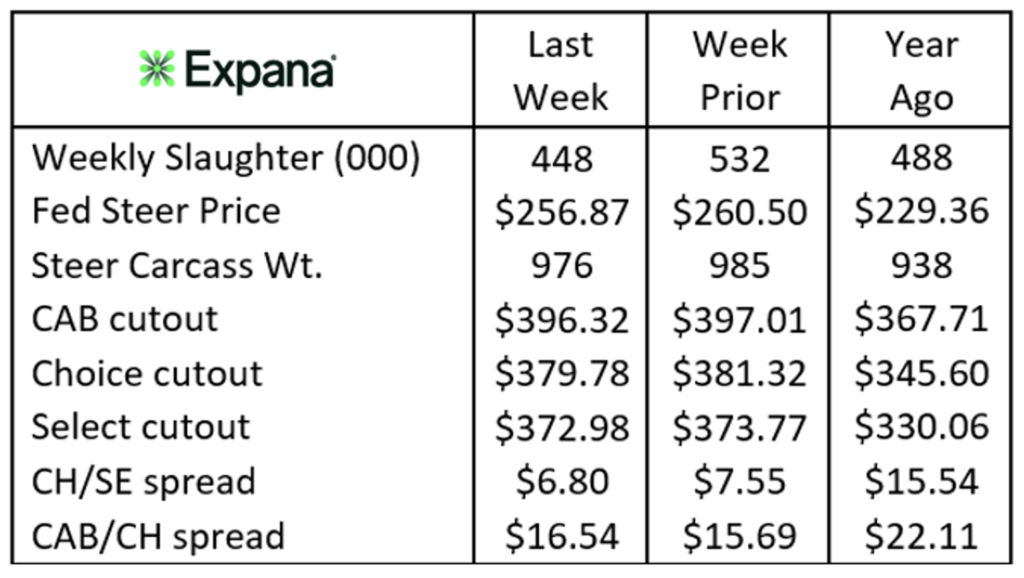

The Memorial Day week curtailed federally inspected harvested head counts last with a 448,000 head total. Late trade on Friday in Nebraska indicated cattle feeders’ firmer stance as many cattle were passed at a significant discount to the prior week’s market. Earlier southern values were recorded between $255 and $257/cwt. although the top of the range was still near $260/cwt. All in all, the market held a notably softer tone in light of very negative packer margins, lower Live Cattle CME futures prices and weaker wholesale cutout values. Not much among these metrics points to stronger fed prices, to say the least.

Carcass weights made a dramatic leap back up to 985 lb. on the steers two weeks ago but immediately readjusted back down to 976 a piece in the latest report for the week of May 11th. The mid-970’s weight range for steers is a positive pullback but we may not see a significant further reduction soon, even though the seasonal trend favors a lower bias into July. Moderate feeding weather and positive feeding margins continue to join with tight supplies to motivate sideways weight outcomes.

Carcass cutout values were slightly weaker last week as wholesale boxed beef movement tended to be lackluster following the holiday. Retail buyers appear to be cautious, slowing their purchases for the time being as they take a wait and see approach. This may be more appropriately classified as a buying strategy rather than indicating softer demand as the buy-side looks for some post-holiday price weakness.

No changes in carcass quality are evident in latest data as USDA Prime continues to run at a nationwide 17% average, led by 21% in Nebraska, and higher on smaller volume in the northeast. Certified Angus Beef ® (CAB®) brand acceptance rates have recently charted a course of 39-40% of all eligible carcasses as average steer weights moved modestly lower, pulling in a small share of cattle below the 1,110 pound threshold compared to heavier average weights recently recorded.

Breaking Down Cutout Values

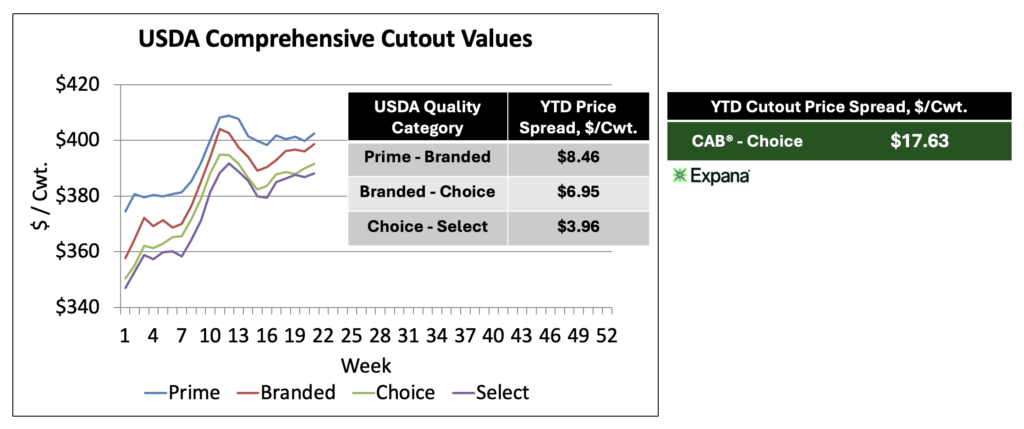

Focused marketing of a premium beef brand demands some attention to tracking price spreads across differing quality specifications. The USDA quality grade scale provides the domestic measuring stick by which the trade differentiates demand across the quality spectrum. Including branded categories like the Certified Angus Beef ® (CAB®) brand to the mix adds complexity to market reporting.

USDA’s “National Comprehensive Boxed Beef Cutout” report (LM_XB463) for all fed steer and heifer product offers a price quote for “Branded Beef.” It’s important to note that “branded beef” in this report consists of any USDA certified brand within any of the quality grades. This price is consequently blended across products with differing marbling requirements and additional specifications, leaving it wanting for more detail. However, USDA’s “National Weekly Boxed Beef Cuts for Branded Product” (LM_XB452) offers a breakdown of cut prices in categories for Upper 2/3’s Choice, Lower 1/3 Choice and Select with nothing specified in branded Prime. In last week’s report the number of loads (weight equivalent to 40,000 lb. loads) in branded Lower 1/3 Choice was 11% of total branded loads while Select loads were 5% of the total, leaving the remaining 84% to Upper 2/3’s Choice brands. While useful to retail end-users, this report likely garners little producer attention and does not summarize total carcass cutout price segregation.

The blended nature of the “branded” category in the Comprehensive Cutout recommends that we use a modicum of caution when referencing this often-quoted price. Consequently, we look to Expana’s CAB® price quote, captured weekly from trade sources, in an effort to specifically delineate the brand premium above commodity Choice. Expana’s quotes are also simple averages, in contrast to USDA’s volume-weighted data. Consequently, the two are not directly comparable even though they reflect the same relative market trends over time.

Armed with an understanding of the peculiarities of these reporting methods, it’s worth noting that the year-to-date average “branded beef” cutout premium above USDA Choice in USDA’s Comprehensive report is $6.94/cwt. At the same time, Expana reports CAB® (traditional, Upper 2/3’s Choice) premium at $17.63/cwt. over Choice. Both data sources are valuable and informative, but are derived from quite different product specifications and weighted differently.

Additionally, “comprehensive” data reporting is quite useful in analyzing beef cut price trends over time. The beef trade, including the Insider Market Update, tends to favor weekly or daily spot market prices. These values get attention because of their “bid and ask” nature of “in the moment” pricing. This lends a feeling of a closer touch to what the retail beef market is demanding. However, just like the fed cattle trade, a majority of beef pricing is formula-based, tied to base spot prices but with quality price spreads factored in for delivery in the future. Comprehensive price data includes all delivery periods, reflecting 100% of the trade volume, both short and long term in nature. As a result, price spreads in the comprehensive report are a reliable guide to what wholesale price relationships are doing while daily spot market price spreads are more headline-grabbing and reactive to what fewer buyers and sellers are doing in a short time span. This factor has recently been demonstrated when the Choice cutout has traded below Select in daily spot trades, reflecting a run on Select product from a buying base finding Select supplies historically tight.

Read More CAB Insider

Seasonal Carcass Impacts

An overriding theme across the past 18 months in the beef sector has been increased carcass weights. In general, fed steer and heifer carcasses averaging 25-30 lb. heavier year over year has been a net positive for the industry.

Rapid Decline in Select Carcasses

The steep upward price trajectory in the fed cattle market remains wholly supported on fed cattle remaining in tight supply and the tight grasp of cattle feeders keeping feedlot stays and carcass weights elevated. Weights continue to underpin beef production tonnage, cutting the harvest pace deficit for fed cattle.

Beef Month Anticipation: Cattle and Beef Values

MARKET UPDATE...