MARKET UPDATE

The last two weeks have brought on a trend reversal in fed cattle prices succeeding the $178/cwt. spring high. Last week’s fed steer price was nearly $3/cwt. lower than the week prior. Most in the cattle feeding sector became quickly convinced that $178 would be the high and it became a self-fulfilling prophecy. With spot market prices at such a premium to futures, there was no holding back hedgers to take advantage of the scenario. Others sold cattle for two-week delivery at prices just below the high.

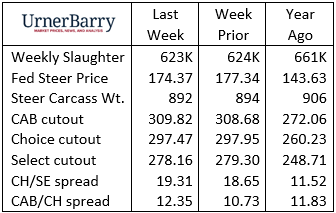

Weekly slaughter is trudging along at a steady pace with fed cattle most recently over 5% smaller than a year ago. No divergence is expected this week.

Boxed beef prices have been under pressure to start beef month as current CAB and Choice wholesale prices are 14% higher than a year ago. Over the past 10 years, cutout values increased on average 6.8% from the first through the third week of May.

A week and a half into May, and there isn’t convincing evidence that a price rally will develop. That’s logical at current price levels and beef buyers appear to be more hand-to-mouth in securing inventory at this time. In the past four weeks comprehensive beef load purchases for 22-60 days out have been down 3.7% compared to the same period a year ago but loads bought for 61-90 day delivery are down 42% in the same comparison.

Carcass quality is holding fairly strong as seasonally appropriate lower marbling scores are noted in USDA grade data. The percentage of Angus-type carcasses eligible for CAB successfully certified into the brand has recently run near 40%. This has been a couple of percentage points higher than a year ago and either side of the historical highs for the period seen in 2021.

Carcass quality of this magnitude is impressive given all that cattle in the northern feeding region endured this winter. As well, the switch from yearlings to the youngest calf-fed steers entering packing plants has effectively pulled marbling achievement down. Price spreads are as strong as ever with the Choice/Select spread over $22/cwt. as of today. Packers are paying an average of $4.83/cwt. on top of Choice for CAB carcasses with the top of the range at $9/cwt. Prime carcasses are averaging $18/cwt. over Choice on the grid with the Prime cutout a $27/cwt. premium to Choice, about $3.69/cwt. lower than a year ago.

As marbling trends lower into May there will be continued premium strength for high-quality carcasses.

VALUE CUTS AND THIN MEATS LEAD

A broad view of recent carcass cutout values shows plenty of strength in wholesale boxed beef prices. To contrast current values to a year ago, CAB and commodity Choice cutouts are 14% higher.

That news comes across rather positive for beef demand but since demand is a function of both price and volume, we must address the caveat. The fed cattle supply year to date has been down through late April by 2.7% but adding the factor of a 17 lb. per head drop in carcass weights pulled fed cattle production down by 5%.

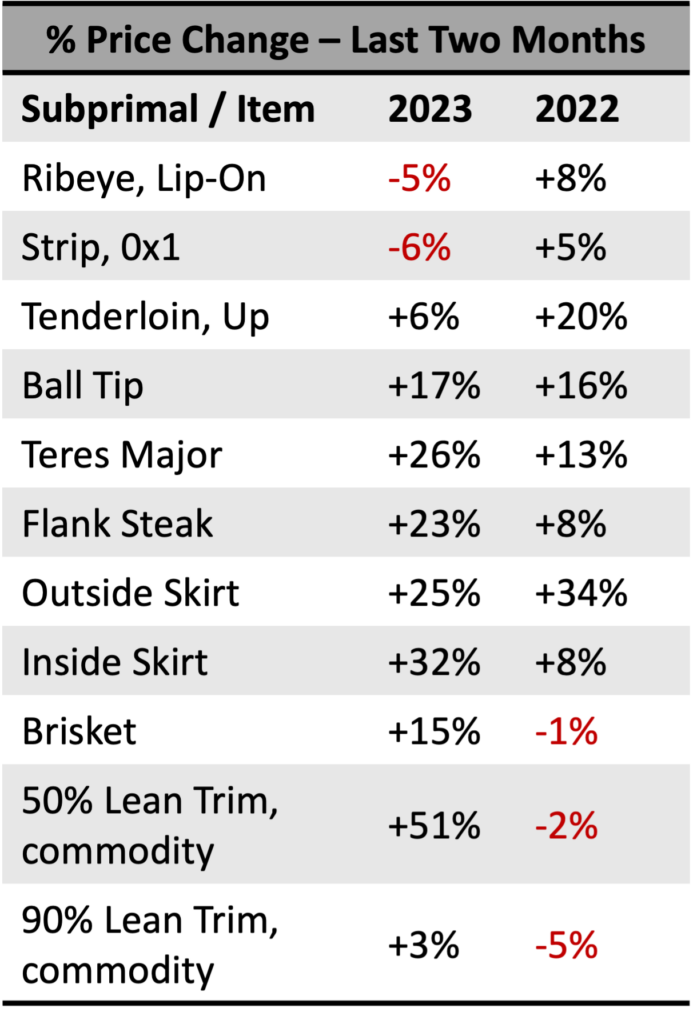

With this perspective there’s more to the demand story looking at price action for various cuts across the carcass. Starting with middle meat steak cuts, demand for ribeyes has been on a downtrend since late March. That’s in-line with last year’s trend but counter to the more common uptick in May with grilling demand. Strip loins deflated from their lofty first-quarter price point but stayed firm in a sideways trend until last week’s uptick to a price near that of last year. Tenderloins, as we’ve mentioned in previous weeks, are the lone ranger in middle meats holding a record-high price since before the first of the year. At $16.00/lb. wholesale, some consumers could view tenderloins as too expensive for purchase.

The “value” steak items are the headline cuts making stronger upward price moves in recent weeks. Ball tips, teres majors and flank steaks are each on a much stronger upward price trend compared to ribs and strips. Flank steaks moved firmly higher in early April and are now matching their $7.95/lb. record-high at wholesale.

Moving on to thin meats (which could include flanks as well) there are exciting prices and stronger trends reported. While export demand has pushed outside skirts to higher trading ranges the spring rally has price soaring rapidly higher on that item. Inside skirts are the secondary skirt item when it comes to price point. But this cut has posted strong spring demand in 2020 and 2021. The current year trend for insides has seen prices ratchet firmly higher since early February, and the line is moving nearly straight up recently.

Briskets are no stranger to late spring demand with volatile pricing best describing the trend in 2021. This season brisket values are not that extreme but are up 15% since late March, adding support to cutout resiliency.

Finally, the all-important ground beef category deserves attention. Cooler spring weather has been a general theme this year and grilling demand may not be pulling product to higher prices just yet. CAB ground chuck is priced right at the 2022 levels currently while ground round and ground sirloin are interestingly lower than a year ago.

On the other hand, 50% lean and 90% lean trim (separate from CAB price quotes) are priced over $2.00/lb. and $3.00/lb., respectively. These are record-high for this time period, excluding the 2020 pandemic volatility.

In summary, current carcass values are being underpinned by positive price moves from several carcass cuts, and we’ve just named a few. The classic spring price rally from ribs is in a counter-seasonal pattern and strips are modestly sideways. End users are seeking value items to partially offset shorter supplies and higher prices.

Read More CAB Insider

Seasonal Carcass Impacts

An overriding theme across the past 18 months in the beef sector has been increased carcass weights. In general, fed steer and heifer carcasses averaging 25-30 lb. heavier year over year has been a net positive for the industry.

Margins Sqeeze, Markets Cool: What It Means for Fed Cattle

Focused marketing of a premium beef brand demands some attention to tracking price spreads across differing quality specifications. The USDA quality grade scale provides the domestic measuring stick by which the trade differentiates demand across the quality spectrum.

Rapid Decline in Select Carcasses

The steep upward price trajectory in the fed cattle market remains wholly supported on fed cattle remaining in tight supply and the tight grasp of cattle feeders keeping feedlot stays and carcass weights elevated. Weights continue to underpin beef production tonnage, cutting the harvest pace deficit for fed cattle.