MARKET UPDATE

The cash fed cattle market trend this summer has been quite positive in relation to history. Prior to the pandemic, cattle feeders could count on cattle supply and beef demand factors aligning to set annual price highs in the spring of the year. April was typically the target month for the high, but realistically any time from April through mid-June would capture the annual high.

So far the 2022 market has followed a relatively flat pricing pattern. Unlike the stereotypical pattern described above, the year-to-date high was posted just two weeks ago with $146/cwt. edging out the spring high of $143/cwt. The relatively late arrival of higher prices continues to be spurred by fewer market-ready, premium grading cattle in the most active cash trading area in the north.

Beef demand is proving to be more resilient than expected. While it is lower than recent years, it appears to be leveling off. Inflationary impacts are certainly a factor as retailers and distributors have held beef prices on a higher plane to accommodate increased input costs.

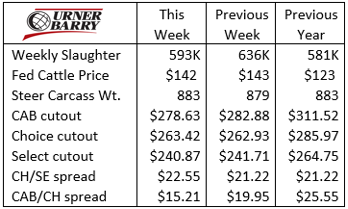

Carcass cutout values have traded in a very stable pricing environment since late April. The Choice cutout has moved little with a range of $257/cwt. to $267/cwt. during that time. Similarly, the CAB cutout has traded from $272/cwt. to $284/cwt. for the period. The latest Choice cutout value is 8% lower than a year ago and the CAB cutout is 11% lower.

As we enter mid-July, lower beef prices are predicted through the dog days of summer. The traditional lower price trend for this period tends to translate into summer lows sought in the market through the first week of August.

Last week’s CAB cutout was slightly lower than the prior week with a $4.25/cwt. decline. Given that May/June wholesale beef prices did not undergo the tremendous spikes seen in the past two years, the transition to July has not generated significant price declines so far. However, ribeyes and strip loins have finally given up some of their June value, as both items were the notably cheaper cuts in last week’s boxed beef trade.

CARCASS WEIGHTS FIND ANNUAL LOW

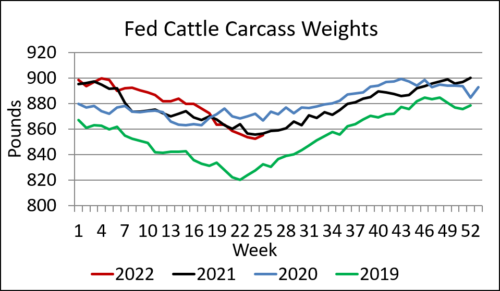

Since the pandemic onset, carcass weights have been on a short list of market-influencing talking points in the cattle sector. It was in May 2020 that national average weights rocketed to as much as 48 lb. heavier than the year before. Since that devastating period, weights have struggled to find significantly lower levels.

A final push of backed-up supplies of fed cattle in the first quarter of 2021 saw carcasses continue to mark new highs. Cattle numbers in the following quarter were brought more current and weights dropped 18 lb. in two weeks to match the weekly average of the year prior.

Jumping ahead to 2022, a slow packing sector pace kicked off January with a quick recovery to more impressive daily harvest levels in February. Carcasses still tracked a heavier path than the prior year from February through early May, finally pulling lower.

The annual average carcass weight low appears to have been made during the week of June 13 with steers averaging 879 lb. and heifers averaging 810 lb. Heifers declined yet another pound in the following week’s data, but steers increased 4 lb. that week to move the average upward again.

Weights now begin their steady climb to their expected November annual heaviest. Reviewing cattle placement in feedlots this year suggests that fewer fed cattle supplies expected in the fourth quarter along with much higher costs of gain will hold carcass weights below a year ago. This will be dependent on the basis trend (cash minus futures price) which guides cattle feeders’ decisions regarding marketing timing.

End-user demand for premium quality grade carcasses remains sharp today, given the premium spreads between grades including CAB carcasses. While impossible to perfectly project carcass values months in advance, the supply/demand evidence we see today suggests that fourth quarter premiums for quality could shape up to be quite strong.

ANGUS YOUTH ACHIEVE CARCASS EXCELLENCE

The National Junior Angus Show, conducted annually in July, is best known as a place where junior Angus members display breeding heifers in the show ring. However, it’s the carcass steer competition, possibly less famous as far as junior cattle shows are concerned, that brought the level of competition to new heights this year.

Forty-two registered Angus steers were harvested in this year’s contest. This exemplary set of cattle graded 30% Prime, 60% Certified Angus Beef ® brand (calculating both Prime and Premium Choice) and just 7% Select. The Prime carcass percentage more than tripled the recent industry average and the CAB share was almost double the brand’s recent average.

The real highlight in this set of steers is the fact that nine head, or 21% of the carcasses, were Prime, YG 2’s. It appears in the data that they would also have qualified for CAB® Prime. It’s a fairly special set of cattle that can hit such a lofty marbling achievement while remaining this lean in terms of their finish, with the Prime, YG’s averaging a mere 0.36 inches of backfat thickness.

Readers may quickly recognize that a backfat measures in commercial fed cattle today are more commonly or well above 0.50 inches. While these steers could have been fed longer in a commercial setting, we might argue that they were fed to their most feed-efficient endpoint in the hands of these junior Angus exhibitors. Our congratulations to this group of exhibitors for setting their sights on excellence and achieving it.

Read More CAB Insider

Seasonal Carcass Impacts

An overriding theme across the past 18 months in the beef sector has been increased carcass weights. In general, fed steer and heifer carcasses averaging 25-30 lb. heavier year over year has been a net positive for the industry.

Margins Sqeeze, Markets Cool: What It Means for Fed Cattle

Focused marketing of a premium beef brand demands some attention to tracking price spreads across differing quality specifications. The USDA quality grade scale provides the domestic measuring stick by which the trade differentiates demand across the quality spectrum.

Rapid Decline in Select Carcasses

The steep upward price trajectory in the fed cattle market remains wholly supported on fed cattle remaining in tight supply and the tight grasp of cattle feeders keeping feedlot stays and carcass weights elevated. Weights continue to underpin beef production tonnage, cutting the harvest pace deficit for fed cattle.