With more global optimism, CAB exports rise in December

MARKET UPDATE

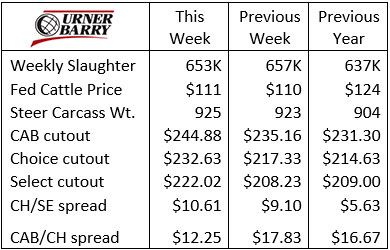

January fed cattle prices traded in a very tight range around $110/cwt. with last week’s CattleFax average steer price up to $112.50/cwt. While this is the highest price on the ledger since the first week of June, the January average price is 12% lower than that of 2020. Cattlemen in all sectors keep looking hopefully toward spring as market-ready cattle supplies shift.

Carcass weights continue to add tonnage to the market on a per-head basis with the latest steer/heifer average 19 lb. heavier than a year ago. Although weights declined in December, they have crept up again to match those seen in late November.

Live Cattle futures are quite unbalanced for the nearby two contract months with a $6.60/cwt. difference favoring April over February. This abnormality affects timing by incentivizing feedyards to push cattle toward later marketing dates.

Cost-of-gain estimates using $5+/bushel corn prices argue the opposite, especially for heavier, more mature cattle, but the cattle futures dynamics are impactful.

Standing in contrast to fed cattle, boxed beef sales are posting serious price gains with the Choice cutout 8% higher than a year ago and the CAB cutout 6% higher. Last week’s price advances were tremendous, with the Choice cutout up $9.44/cwt. in 7 days and cutout values second only to those seen in 2015 for that week.

Starting out February with such a strong spot market is uncharacteristic. We’ve noted this period tends to be the weakest beef-demand month of the year, but that’s not the current picture. When we consider the large slaughter head counts plus the tonnage increases due to carcass weight, this is really a high-water mark for demand.

Many states with the worst COVID-19 conditions and the most restrictive restaurant dining policies are just now beginning to open up foodservice for dine-in business. Even though occupancy policies are in place, many people haven’t had the opportunity to eat in a restaurant for a very long time. Some of the current demand spike is due to that recent further opening of the foodservice sector.

WITH MORE GLOBAL OPTIMISM, CAB EXPORTS RISE IN DECEMBER

When cattle prices and producer sentiment are lackluster, sometimes it’s nice to look to a bright spot in the market. At CAB, a recent snapshot of December export data provides some interesting fodder, and something to get excited about.

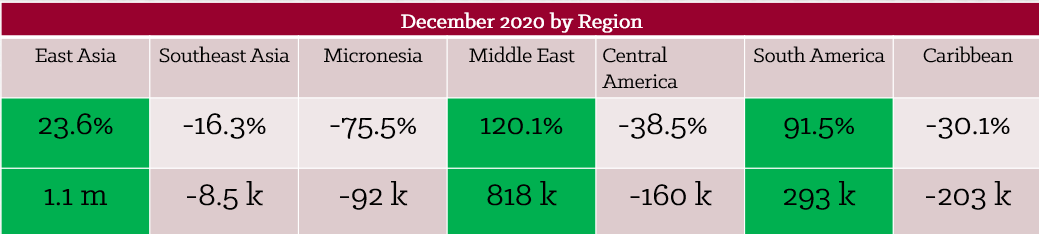

December saw growth in 8 out of 10 of the top CAB export markets based on tonnage, as compared to 2019 figures for the same timeframe. CAB is sold in 51 countries outside the U.S. and adding up sales across the board, December is up 14.4 million pounds (lb.) or 11.8%.

It should be noted, December 2019 was a softer-than-normal month due to market factors such as the Tyson plant fire earlier that year. But nonetheless, there’s reason to find optimism in current demand outside of our borders.

Kuwait and the United Arab Emirates led growth, so a regional breakout shows the Middle East up 120% over the previous December. Our international team notes that although precautions are still being taken, distribution in this region is almost “business as usual.” The brand will add more distribution channels across the Middle East in the very near future.

South America is up 91%, with strong partners in Peru, Chile and Colombia, where a shift to retail and e-commerce helped bolster sales.

East Asia posted a 23.6% growth, led by steadily higher sales in Japan at 2.6 million lb. and South Korea at 1.6 million. However, Hong Kong and Taiwan had even larger percentage growth, showing up as considerable buyers in the market. China does not make the top 10 yet, but the purchasing power and desire for more U.S. beef is there. Logistics and sourcing enough ractopamine-free cattle are current hurdles.

The hardest hit among top CAB export markets is Canada, where retail demand is strong, but foodservice business has suffered immensely from the lockdowns this winter. Sales there are down 18%.

Historically, high-quality beef demand in leading export markets has relied on tourism, and in places like the Caribbean, the Dominican Republic and Mexico, it still does. Yet, there’s a growing shift to complement that tourism-related buying with true domestic retail demand in many countries. They are showing an appetite for quality.

During this period, CAB personnel have not been able to be the “boots on the ground,” delivering typical in-person trainings and sales meetings. However, they stayed involved with customers via creative virtual sessions and addressing specific needs in specific regions. The enthusiasm from the buyer side is good anecdotal evidence this one-month export improvement will build on itself throughout 2021.

DON’T MISS THE LATEST HEADLINES!

CAB brand basics

Select beef: Who wants it?

Driving demand: Retail

Read More CAB Insider

It’s Beef Month

Wholesale and retail beef buyers have been preparing for weeks ahead of the spike in consumer beef buying associated with warmer weather and holiday grilling demand.

USDA Prime Eclipses Select

In a twist unthinkable just two decades ago, USDA data reveals that the current percentage of Prime carcasses has averaged 11.9%, surpassing Select carcasses that are averaging 11.1%, in each of the last five weeks.

Carcass Quality Spreads Pop

High quality steak and roast items such as ribeyes, strip loins, tenderloins and sirloins carry an outsized share of the load when it comes to generating pricing separation up and down the carcass quality spectrum.