Select carcass value pressure

MARKET UPDATE

The fed cattle price recovery that has been painstakingly built since early September has eroded in an extraordinary decline over the past two weeks.

All facets of the beef supply chain have acknowledged the fed cattle supply burden we face as we begin the new year. However, it seems that the fund managers just became enlightened to that reality, rapidly reducing long-hedged positions and creating the waterfall effect.

Unfortunately, this has not only chipped away the December and February Live Cattle contracts (the two months correlated to this near-term oversupply), but adjusted every contract month on the board. Fortunately, Tuesday of this week saw at least a momentary stabilization, as positive contract prices emerged.

Cattle futures direction, coupled with the December corn futures price near $4.15/bushel, has generated a similarly fast redirection in feeder cattle and calf prices at auctions. Producers merchandizing their spring calf crop the second week of October were likely relatively pleased with the outcome, while those marketing in the subsequent week were handed a difficult dose of reality. Volatility is alive and well.

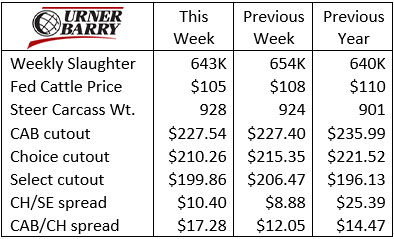

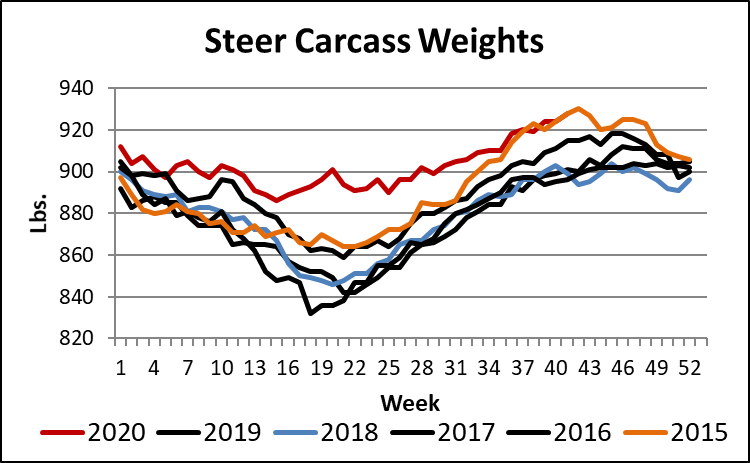

One aspect that we just can’t ignore as we enter November is carcass weights. Fed steer carcasses in the latest confirmed data were 27 lb. heavier than a year ago; history suggests the annual heaviest weights will be marked in mid-November. Winter weather and near-record cold temperatures this week in the western section of the cattle feeding belt will likely help to slow the uptick. Weekly beef tonnage remains aided by heavy carcasses, as head counts bounce from below to above year ago levels weekly.

The comprehensive beef cutout value came down more than $5.00/cwt. last week. This should work in favor of beef demand and product movement. However, lower cutout values signal some recent resistance from end users at the price points higher than where the market is today.

Quality spreads in the beef offering widened up a bit last week as the Certified Angus Beef ® brand cutout remained essentially unchanged, while Choice slipped $5.09/cwt. and Select fell $6.61/cwt. Note the magnitude of the spreads with CAB/CH at $17.28/cwt. and CH/SE at $10.40/cwt.

Select carcass value pressure

High-quality, premium branded beef products would offer little value to the production sector in the absence of price differentiation. The fact that premiums exist and opportunities to charge more for higher quality are the drivers of the system.

For decades the beef supply chain has factored the Choice/Select price spread as the standard by which we measure demand for beef cuts. A wider spread signals strong demand from the market for marbling while a narrow spread suggests weaker demand for the same.

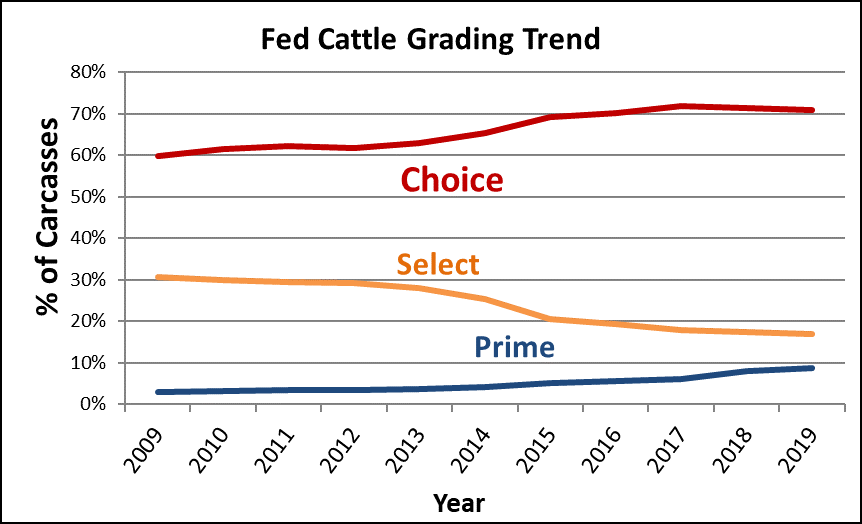

We don’t often focus on the Select carcass trends but it’s informative to do so in the face of shrinking supplies in that category. Over the past decade alone, Select carcass production has fallen by nearly 50% in relation to Choice and Prime. So far in 2020 the Select proportion has been 13.8% of fed cattle carcasses, following the 2019 total of 16.9%.

Realizing that Select supplies have dramatically declined is important as we look at demand for Select beef. Price and volume are the two drivers that define demand.

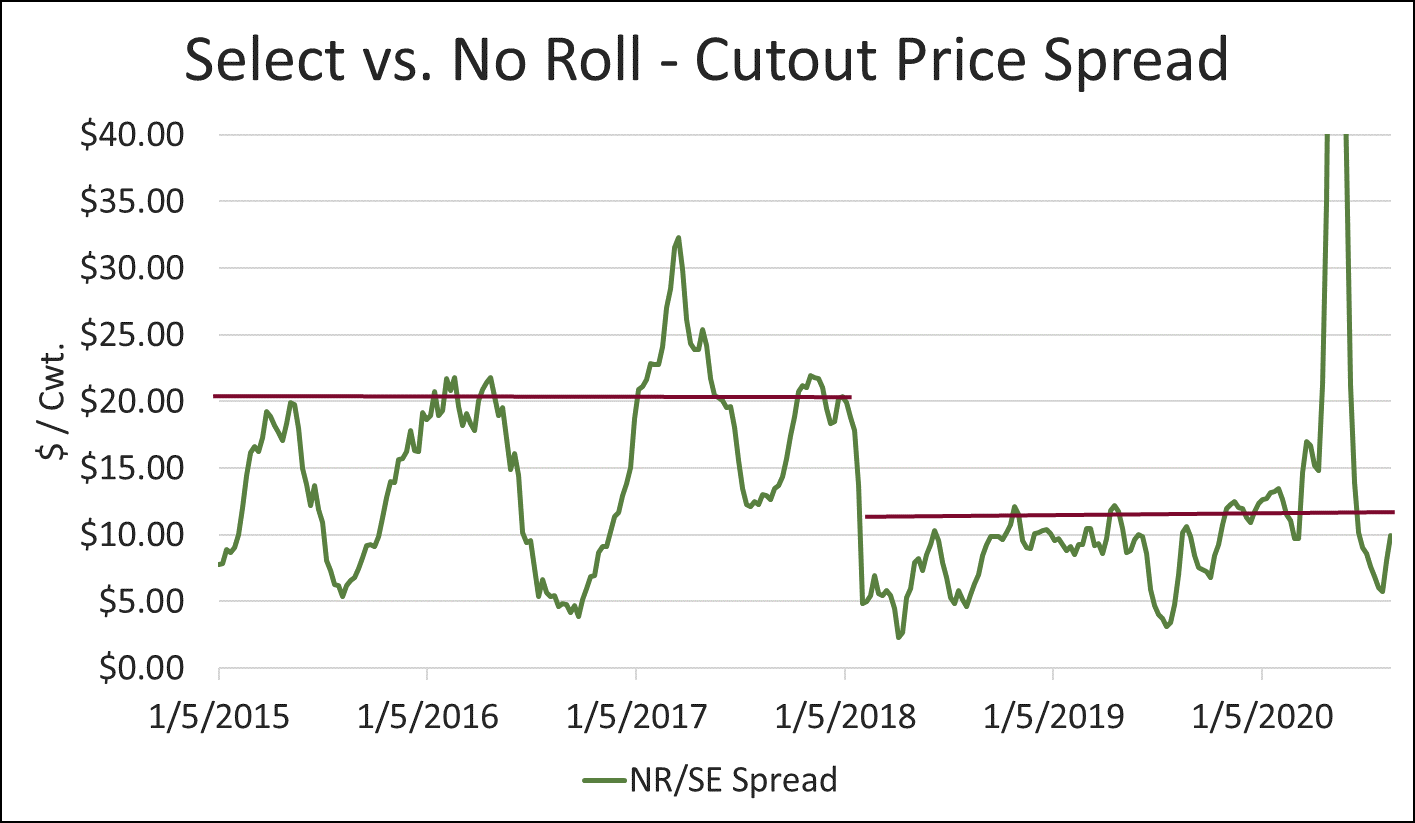

With Select supplies becoming smaller and smaller, we might assume that scarcity could drive prices higher, given healthy demand. The chart, below, doesn’t specifically define demand for Select beef but it does show an interesting relationship between Select and No Roll carcass cutouts. No Roll carcasses are those that are practically devoid of marbling, consequently not receiving a grade at all. The chart shows that during the past two years, with the exception of this May, the spread between Select and No Roll carcasses has narrowed. Highs in that price spread that previously touched $20/cwt. were reduced to $12/cwt. beginning in 2018. The lows in the comparison are also slightly lower in more recent years, while the range from highs to lows has also narrowed.

This suggests that Select grade beef products are being met with less and less demand. The U.S. retail sector can be credited with embracing higher marbling beef products. Not only has Choice surpassed 70% of the fed cattle supply but the Certified Angus Beef ® brand is often 20% of the total, while Prime has been as high as 12%. Greater availability of the premium beef products is key to retailers’ ability to feature high quality beef and count on a consistent supply in volume.

With Select product devalued to this extent and representing a shrinking category, we need to embrace the change. Low Choice is no longer a premium, but the low water mark. Producers and end users alike should begin their beef quality conversations with premium Choice and Prime branded products with specifications. This is the “new normal” and the key to demand today and tomorrow.

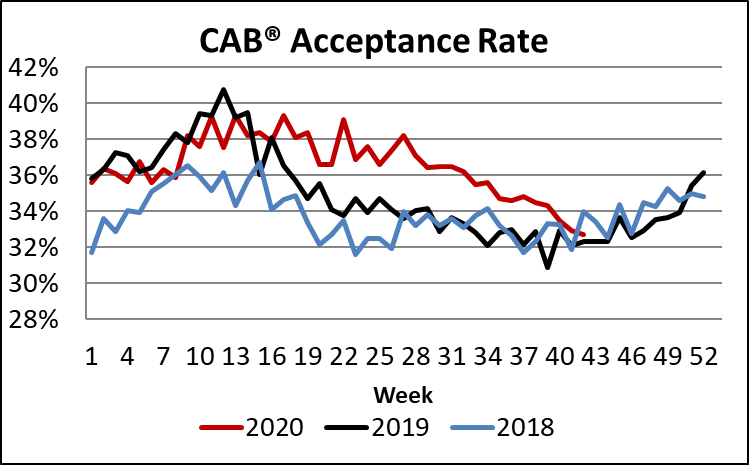

CAB carcass acceptance nears annual low

As fed cattle carcass weights push toward the record highs seen in November 2015, we might assume that premium quality grades will follow the trend higher, also setting annual highs. Certainly, Choice and Prime grades are currently at record levels this year, in conjunction with abnormally high carcass weights. While there is a correlation, the causation is most likely tied to days on feed, rather than carcass weight alone. This is evidenced by the rapid fall increase in carcass weights and simultaneous decline in the Choice and Prime grading percentage.

Industry-sourced data shows that the number of cattle on feed for 150 days or longer declines precipitously from June through October. That trend is even more evident given the abnormalities of 2020.

Specific to the CAB® brand, as carcass weights top out in the fall we tend to see more carcasses that would otherwise qualify for the brand deemed unacceptable due to surpassing the 1,050 lb. carcass weight limit and/or exceeding the 16 square inch maximum ribeye size.

Finally, with average days on feed declining to near annual lows, the proportion of the Choice carcasses with enough marbling to achieve the brand’s requirement for mid-Choice or higher marbling is a limiting factor.

A declining proportion of CAB carcasses in the mix gives rise to opportunities for cattle marketers in the fourth quarter, as grid premiums tend to increase for high-quality cattle as heightened demand meets marginally smaller supplies.

DON’T MISS THE LATEST HEADLINES!

CAB momentum

Flavor’s secret ingredient

Keeping up

Read More CAB Insider

Onward with Quality

It’s been a quality-rich season in the fed cattle business with added days on feed and heavier weights continue to push quality grades higher.

It’s Beef Month

Wholesale and retail beef buyers have been preparing for weeks ahead of the spike in consumer beef buying associated with warmer weather and holiday grilling demand.

USDA Prime Eclipses Select

In a twist unthinkable just two decades ago, USDA data reveals that the current percentage of Prime carcasses has averaged 11.9%, surpassing Select carcasses that are averaging 11.1%, in each of the last five weeks.