MARKET UPDATE

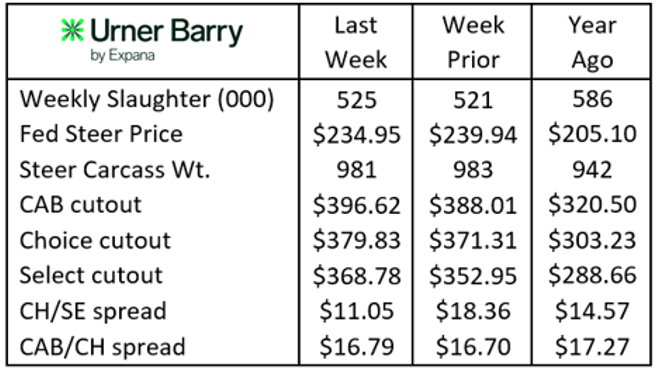

Cash fed cattle values have been under pressure from several factors over the past two weeks. The Iranian conflict began overshadowing equity markets earlier this month, while that general market uncertainty spilled over to Live Cattle futures, negatively impacting cash values. Just as importantly, continuation of smaller weekly cattle harvest volumes have given packers a measure of pricing power over feedyards for the period. Finally, the strike at the JBS-Greeley packing facility, initiated last week, is a headwind in the region as JBS redirects cattle to its other plants. These combined factors have seen prices retreat from $243/cwt. two weeks ago to last week’s $234/cwt. average. Despite this, Live Cattle futures posted gains Monday and Tuesday.

Carcass weights remain heavy, relenting just 8 lb. lower than the December record-high in the latest report. In the last five years, steer carcass weights have declined 16 lb. from the beginning of January through mid-March, on average. This year, steer weights have declined by only 4 lb. for the period. While 2026 fed cattle supplies are estimated to be the lowest in the cycle, it appears that the feedlot sector is, ironically, becoming less current on market-ready cattle inventory.

Carcass cutout values have followed the opposite trajectory to that of cattle, with last week’s sharp upticks adding punctuation to increases building in prior weeks. Beef demand continues to hold strong with the “All Fresh” retail beef price at a record $9.64/lb. in February. Price increases in March are in line with the seasonal trend, but the 30-cent-per-lb. rise from mid-February through last week is more pronounced than similar patterns in recent years. Undoubtedly, limited cattle harvest throughput and the onset of early spring beef demand have combined to spur the increase.

Quality Soaring Higher

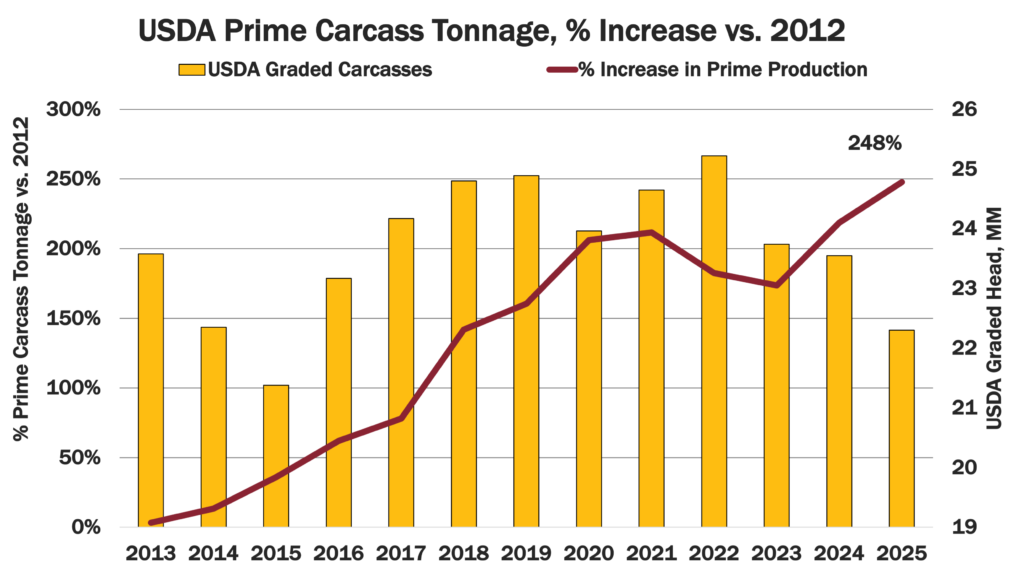

The 2025 U.S. annual average share for Prime carcasses set a new high watermark at 11.9% of fed cattle. While not a formidable percentage compared to USDA Choice at 72% of the mix, growing supplies in the Prime category have been transformational for the beef industry. With Prime historically relegated to just 2-3% of total fed cattle supply, it began it’s rise in 2013 with incremental annual increases.

The contrast is starker by illustrating the change in Prime carcass tonnage over this short timeline. First, we must factor in carcass weights, which were 85 lb. heavier in 2025 than in 2012, the last year that Prime comprised a 3% or less share. The Prime production increase was not linear over this period, yet has made a convincing overall move, generating 263% increased carcass tonnage in 2025 compared to 2012.

As if this weren’t enough, the Prime category has soared at a renewed pace since last September. Beef stakeholders rightly assumed that the Prime grade would continue to perform, given the current weather and feeding sector economics. Yet, the pace of the increase has likely outpaced most guesses, as the Prime grade has not charted below 14% of the grade mix so far in 2026.

March tends to be the month with the richest marbling, as both CAB and Prime percentages peak at this time. The month started with a highlight well outside the trend, with USDA reporting that Nebraska packers averaged 24.3% Prime across their harvest in the first week of the month. The nearly 7% increase over the prior week is staggering enough to raise questions. However, with carcass weights remaining record-heavy for this time of year (32 lb. heavier than a year ago), one must embrace new possibilities.

Ultra-heavy carcasses and extended feeding days are a double-edged sword for the Certified Angus Beef ® brand. The richer marbling trend increases the share of eligible carcasses that meet the Modest 00 or higher requirement. Yet moderate slippage of carcasses above the 1,100 lb. maximum, plus a few with backfat above the 1-inch limit, are the most noted of the other specifications capping growth in brand acceptance rates currently.

Increased Prime carcass production is a boon to sales growth in this category for both Certified Angus Beef and the industry as a whole. A smaller Prime cutout premium above Choice also means greater adoption of this premium product tier by grocers and restaurants. All of the above lead to a firmer foothold for beef as the protein of choice for consumers.

Read More CAB Insider

Utilization Key to Prime Success

More demand for individual Prime grade cuts is being discovered on the part of packers and wholesalers as they educate downstream users about the opportunities to capitalize on growing Prime demand.

Seasonal Demand Shifts Carcass Values

January often presents the lowest beef demand, while February likely vies second. Also, we see a shift in consumer preference away from holiday middle meat roasts toward end cuts for “comfort food” meals.

Price Speaks Volumes

While the tightest fed cattle supplies in the cycle are projected this year, consumer demand has issued directional support that tight supplies do not necessitate narrowing of price differentiation for quality.