MARKET UPDATE

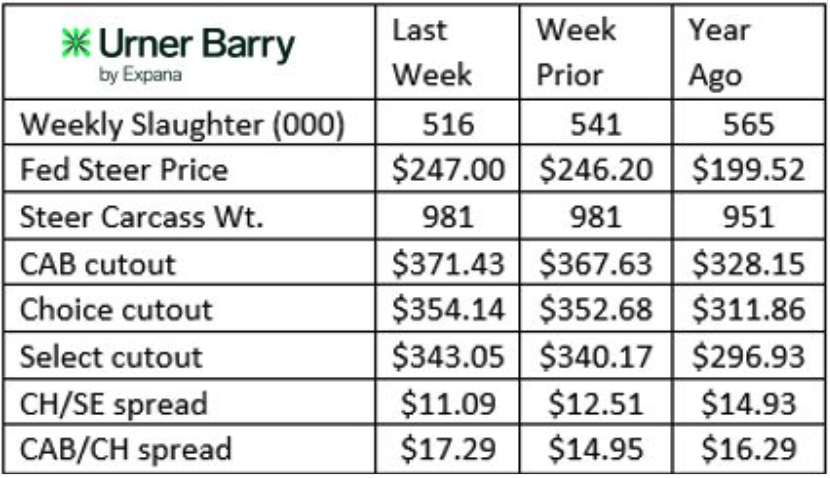

The fed cattle market continued to show strength last week as negotiated trade developed very late on Friday. February Live Cattle futures traded near contract highs at $247/cwt. and small cash trade volume in the north centered on that price.

Extremely small harvest volume was the key element in last week’s market, sending a clear message that packer margins—near $300 per head— in the red— have forced reductions on throughput Granted, Monday’s President’s Day was a federal holiday, but this is negated as a consideration for harvest volume, as packer capacity for the week was sharply underutilized.

Friday’s Cattle on Feed report proved uneventful as analyst expectations were met with the number of cattle on feed in feedlots (with at least 1,000 head of capacity) at 98.2% of a year ago. January marketings look quite low at 87% of a year ago, but there was one fewer marketing day this January. With that said, a smaller cattle harvest is evident with year-to-date figures at -5.8%.

Carcass cutout values showed some life with slightly higher values last week on a steadily higher trajectory. Mixed price direction has recently been a theme across the major carcass primals. Firming demand for round cuts is the most notable trend in recent days, as utilization of lean, grinding beef is cropping up again. With spring spot market demand in the forward view, ribeye prices were a bit higher, but they are just trading off of their winter lows.- Wholesale strip loin prices have adjusted lower after making strong moves to the upside throughout January into early February.

Protein Price Spreads

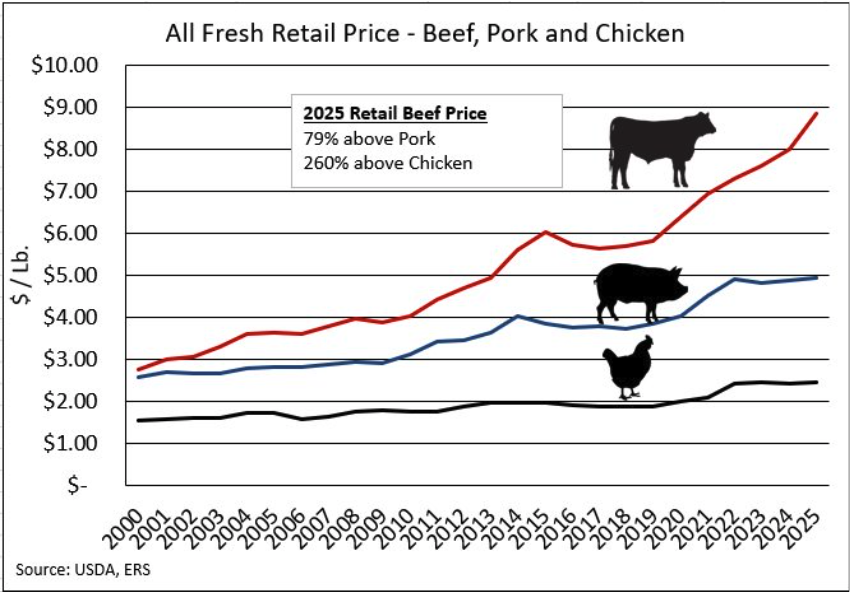

The inflationary theme in the grocery sector is impossible to miss, as most Americans are faced with the buying a large share of their food at retail. Beef has been in the media crosshairs for months as retail prices have escalated. The “all fresh” retail beef price increased 10% from 2024 to 2025, with another 6% the prior year. Yet consumers have a choice in meeting their protein needs, and they continue to demand beef at an impressive level. In fact, beef demand in the fourth quarter of 2025 was record-high, according to analysts at Terrain.

A simpler approach is to realize that U.S. per capita beef consumption was nearly unchanged in 2025 at 58.4 lb., scarcely lower than the 59 lb. in 2024. Couple that with the 10% average annual retail price and one can quickly see that demand was robust.

Even more amazing: Beef has built a rapidly widening price gap over competing meats in the grocery store. This trend has become increasingly pronounced since the early 2000s, but as beef supplies have tightened over the past three years, the pace of the widening price disparity has accelerated.

During 2022, the peak of the cycle’s largest beef supplies, retail beef prices were 49% higher than pork and 200% higher than chicken. This is a large contrast to the 2025 average, with beef pricing 79% higher than pork and 260% higher than chicken. It’s important to note that beef retail prices rose rapidly throughout 2025 as the fourth quarter’s $9.44/lb. average was 13.8% higher than the first quarter average. Once again, the fourth quarter saw record beef demand despite rapidly escalating prices.

Market analysts point to evolving consumer attitudes toward meat as an important component of a healthy diet. The popularity of GLP-1 medications (with meat indicated as a healthy protein source) and the recent inversion of the USDA food pyramid are contributing factors. Consumers may be adapting to the nutrient density and wholesomeness of beef as they compare the return on their grocery dollar to less healthful food options.

It’s imperative to credit beef quality advancement in the consumer behavior discussion. The beef industry is offering consumers the most satisfying eating experience they’ve ever encountered, as the share of USDA Prime and Certified Angus Beef ® brand product continue to swell as a portion of fed cattle production. This leaves little doubt that marbling-rich carcasses are driving beef to outperform other protein sources in the meat case.

Read More CAB Insider

Choice-Select Spread Inverted

MARKET UPDATE...

Quality Soaring Higher

Increased Prime carcass production is a boon to sales growth in this category for both Certified Angus Beef and the industry as a whole. A smaller Prime cutout premium above Choice also means greater adoption of this premium product tier by grocers and restaurants. All of the above lead to a firmer foothold for beef as the protein of choice for consumers.

Utilization Key to Prime Success

More demand for individual Prime grade cuts is being discovered on the part of packers and wholesalers as they educate downstream users about the opportunities to capitalize on growing Prime demand.