MARKET UPDATE

Regardless of which market we might discuss, “uncertainty” is an accurate descriptive term. U.S. equities are unsettled with interest rate hikes currently delayed but promised in March, according to the Federal Reserve.

This background has done little to settle the equity markets, and this spills over to cattle and beef. A couple of strong days headlined cattle futures this week, following up a very choppy futures trade a week ago.

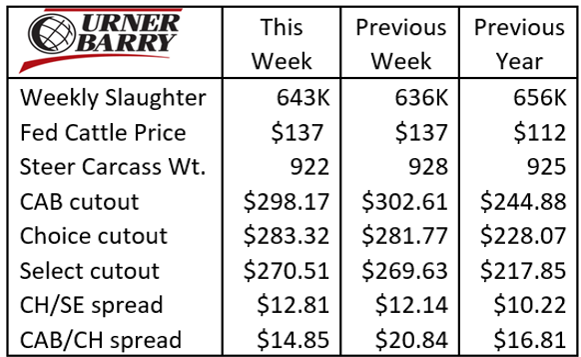

Cash cattle trade this Tuesday found feedyards fairly bullish and packers equally responsive in the range of $140/cwt. Trade was regional at this price, but the $3/cwt. increase over last week’s average found feedyards willing to sell their better cattle.

A broader view of fed cattle prices for January reveals a sideways price trend, with very little tie from boxed beef values to fed cattle prices.

Packer efficiency improved last week, with an incremental uptick in the slaughter pace to 643K head, a 1.1% increase over the prior week. As we’ve reiterated many times before, larger slaughter rates are key to the success of every supply chain sector. There is no downside to larger head counts at this time.

The historical bias for beef demand for the month of February is lower. As a matter of fact, Feb. tends to be the low-demand month of the year. We can practically throw this aside in 2022 because of the smaller harvest pace.

Beef inflation is a two-pronged anomaly today. Of course, the broader economy is reflecting the inflationary conditions across all consumer goods. Yet retail beef prices continue to bear the added burden of the imbalance in supply and demand.

Boxed beef values last week were mixed, with the CAB cutout reported slightly lower but Choice and Select values a bit firmer. Early this week, the daily pricing shows a softer pricing trend across the board. Two primary factors are continued concerns of COVID and the fact that current retail beef price levels are record high for this time of the year, 20% higher than the same period last year. Regarding COVID concerns, end users are likely debating that normal Valentine’s Day beef demand will be lessened.

COW HERD IMPLICATIONS

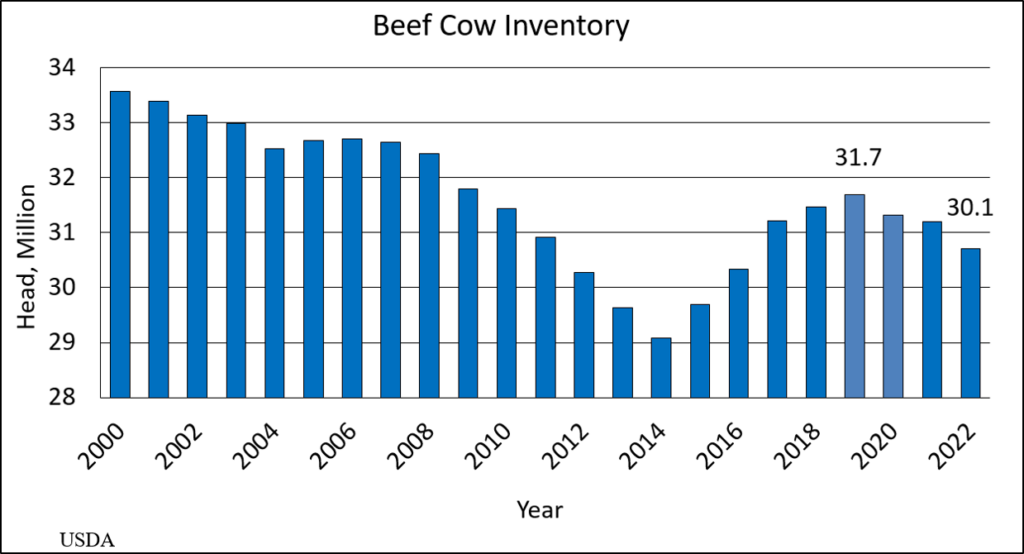

The USDA January 1 cow herd inventory, published this Monday, confirmed a 2% decline in the beef cow herd, along with a 1% decline in feeder cattle supplies. This is relatively in line with earlier estimates, although some had projected the beef cow decline fractionally smaller than the USDA number.

Implications moving forward for cattle markets remain unchanged due to this report, as these facts were already priced in to the market. Good news for cattlemen from a price perspective, as the outlook is quite bullish with smaller supplies expected to heat competition for feeder cattle. As we’ve noted, feeder and fed cattle futures contracts in the deferred months have priced this in for some time now.

In the near term, placements of feeder cattle have been robust in the fourth quarter and January is likely to show another strong month of placements. For the 2022 marketing year, this has front-loaded the calendar year with cattle directed more heavily toward feedlots. Fewer are going out to graze on small grain pastures due to dry conditions.

The second half of the year has risk toward fewer fed cattle supplies in terms of the typical seasonal balance. Of course, this has opposing implications for buyers and sellers of fed cattle during that period.

Read More CAB Insider

Credit End Meats With CAB Value-Add

We focused on fourth-quarter middle meat demand as a beef price driver in the last edition of the Insider. This is certainly the case in the current data as rib and tenderloins are pricing near their annual highs. However, a look at annual price trends across the beef carcass shows increasing contributions to CAB premiums from both ends of the carcass.

Middle Meats and Supply Driving Fourth Quarter Spreads

At the retail level, November brings a brief shift in focus, away from beef to turkey and ham, for Thanksgiving meals. Turkeys are the classic “loss leader” item in grocery stores during November as retailers practically give them away to lure a volume of shoppers to spend on the high-margin center of the store goods.

CAB Brand Sales Third Best in 45-Year History

In this CAB Insider,shifting market dynamics have already marked trend changes in the 2023 cattle and beef markets. These shifts are most succinctly summarized through two factors, fewer cattle and higher prices, that will further entrench themselves in near term trends.